Securing funding for your small business can feel like navigating a complex maze. Understanding the various small business loan options available is crucial for success. From traditional bank loans to innovative online platforms, the landscape offers diverse avenues to access capital, each with its own set of advantages and disadvantages. This guide aims to demystify the process, empowering you to make informed decisions and choose the best path for your unique business needs.

We’ll explore the different loan types, eligibility criteria, application procedures, and key factors to consider when selecting a lender. We’ll also delve into the importance of a strong business plan, credit score, and effective cash flow management in securing and repaying your loan. Ultimately, our goal is to equip you with the knowledge to confidently navigate the world of small business financing and achieve your entrepreneurial goals.

Types of Small Business Loans

Securing funding for your small business can be a crucial step towards growth and success. Understanding the different types of loans available is essential to choosing the option that best fits your specific needs and financial situation. This section will Artikel several common loan types, highlighting their features, eligibility criteria, and typical interest rates.

Term Loans

Term loans provide a fixed amount of money upfront, repaid over a predetermined period with regular, scheduled payments. These payments typically include both principal and interest.

| Loan Type | Description | Eligibility Requirements | Typical Interest Rates |

|---|---|---|---|

| Term Loan | Fixed amount, repaid over a set period with regular payments. | Good credit score, established business history, collateral may be required. | Varies greatly depending on creditworthiness and loan amount; typically 6-15%. |

A term loan is ideal for purchasing equipment, renovating a space, or covering significant one-time expenses. The advantage is the predictable repayment schedule; however, a disadvantage is the potential for higher interest rates compared to other options if your credit isn’t strong. For example, a bakery needing to buy a new oven might find a term loan beneficial.

Lines of Credit

A line of credit functions like a revolving credit account, allowing you to borrow money up to a pre-approved limit. You only pay interest on the amount you borrow, and you can repeatedly borrow and repay within the credit limit.

| Loan Type | Description | Eligibility Requirements | Typical Interest Rates |

|---|---|---|---|

| Line of Credit | Revolving credit with a pre-approved limit; pay interest only on borrowed amount. | Good credit score, established business history, may require collateral. | Variable rates, generally higher than term loans but lower than some other options; typically 8-18%. |

Lines of credit are best for businesses with fluctuating cash flow needs, such as seasonal businesses or those with unpredictable expenses. The flexibility is a major advantage, but the variable interest rates can be a disadvantage if rates rise. A landscaping company experiencing busy seasons followed by slower periods might find a line of credit beneficial for managing cash flow.

SBA Loans

Small Business Administration (SBA) loans are government-backed loans offered through participating lenders. They typically offer more favorable terms than conventional loans, such as lower interest rates and longer repayment periods.

| Loan Type | Description | Eligibility Requirements | Typical Interest Rates |

|---|---|---|---|

| SBA Loan | Government-backed loans with favorable terms. | Meets SBA eligibility criteria (e.g., business size, purpose), good credit history, business plan. | Lower than conventional loans; rates vary depending on loan type and terms. |

SBA loans are suited for larger capital expenditures or significant business expansion. The lower interest rates and longer repayment periods are major advantages; however, the application process is often more complex and time-consuming. A startup technology company seeking funding for research and development might benefit from an SBA loan.

Microloans

Microloans are small loans, typically under $50,000, designed for entrepreneurs with limited access to traditional financing. They are often provided by non-profit organizations or community development financial institutions (CDFIs).

| Loan Type | Description | Eligibility Requirements | Typical Interest Rates |

|---|---|---|---|

| Microloan | Small loans for entrepreneurs with limited access to traditional financing. | Business plan, credit history (though often less stringent than other loans), may require personal guarantee. | Can vary significantly, but often higher than other loan types. |

Microloans are perfect for startups or very small businesses with limited credit history needing seed capital. The accessibility is a key advantage, but the higher interest rates and smaller loan amounts can be disadvantages. A home-based artisan needing funds to purchase supplies might find a microloan helpful.

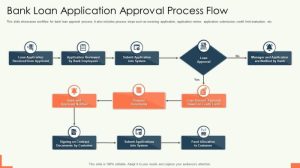

Eligibility and Application Process

Securing a small business loan hinges on meeting specific eligibility criteria and navigating the application process effectively. Understanding these aspects is crucial for increasing your chances of approval. This section details the typical requirements and provides a step-by-step guide to help you through the application process.Eligibility requirements vary depending on the lender (banks, credit unions, online lenders, etc.) and the type of loan.

However, common factors considered include credit score, business history, and financial stability.

Typical Eligibility Requirements

Lenders assess several key factors to determine your eligibility. A strong credit score is often a prerequisite, demonstrating your responsible financial management. The length and stability of your business’s operational history are also important, showcasing your experience and track record. Furthermore, lenders examine your financial statements (profit and loss, balance sheet, cash flow) to assess your business’s financial health and its ability to repay the loan.

Finally, the purpose of the loan and the proposed use of funds are scrutinized to ensure a viable business plan. For example, a loan application for expanding an already profitable bakery will likely receive more favorable consideration than one for starting a business with an untested concept and no revenue history.

Step-by-Step Application Process

The application process generally follows these steps. First, you’ll need to identify your financing needs and research potential lenders. Next, you’ll pre-qualify with lenders to get an understanding of your loan options and required documentation. Then, you will complete a formal application, providing all necessary documentation. After submission, the lender will review your application and may request additional information.

Upon approval, you will negotiate the loan terms and sign the loan agreement. Finally, the lender will disburse the funds. Delays can occur at any stage, especially if documentation is incomplete or if further verification is needed.

Required Documentation Checklist

Preparing all necessary documentation beforehand significantly streamlines the application process. A complete application package typically includes:

- Personal and business tax returns (several years’ worth)

- Business plan outlining your business’s goals, market analysis, and financial projections

- Financial statements (profit and loss statement, balance sheet, cash flow statement) for the past few years

- Personal financial statements, including bank statements and credit reports

- Business licenses and permits

- Resumes of key personnel

- Collateral information (if required, such as property or equipment ownership)

Having these documents readily available saves time and improves the efficiency of the application review. Remember that the specific requirements may vary depending on the lender and the loan type. Always confirm the exact documentation needed with your chosen lender before submitting your application.

Impact of Business Factors on Loan Approval

Securing a small business loan hinges significantly on various factors related to your business’s financial health and operational stability. Lenders assess these factors to determine the likelihood of loan repayment and the overall risk involved. A comprehensive understanding of these factors is crucial for improving your chances of loan approval.

Strong Business Plan’s Influence on Loan Approval

A well-structured business plan serves as a roadmap for your business, demonstrating your understanding of the market, your target audience, and your financial projections. Lenders view a strong business plan as evidence of your preparedness and commitment. It Artikels your business’s goals, strategies, and financial forecasts, providing lenders with the confidence that you have a clear path to profitability and can repay the loan.

A compelling business plan includes detailed market research, a comprehensive competitive analysis, a realistic financial projection, and a clear explanation of how the loan will be used to support business growth. Without a robust plan, lenders may perceive a higher risk and be less likely to approve your application. For example, a plan showcasing a unique selling proposition, a well-defined target market, and a detailed financial model showing positive cash flow within a reasonable timeframe is far more persuasive than a generic or poorly researched plan.

Credit Score and Business History’s Impact on Loan Approval

Your personal and business credit scores play a pivotal role in loan approval. A high credit score indicates responsible financial management and reduces the lender’s perceived risk. Lenders often use credit scores to assess your creditworthiness and predict your likelihood of repaying the loan. Similarly, a strong business history, demonstrated through consistent revenue, profitability, and timely payment of debts, significantly enhances your chances of approval.

A consistent track record of successful business operations provides evidence of your ability to manage finances effectively and maintain profitability, thereby mitigating the lender’s risk. For instance, a business with a consistently positive cash flow for the past three years and a spotless payment history is considerably more attractive to lenders than a newly established business with limited financial history.

Collateral and Personal Guarantees in Securing a Loan

Collateral and personal guarantees act as safety nets for lenders, reducing their risk in case of loan default. Collateral refers to assets you pledge as security for the loan, such as real estate, equipment, or inventory. If you fail to repay the loan, the lender can seize and sell the collateral to recover their losses. A personal guarantee, on the other hand, involves a personal commitment to repay the loan if your business is unable to do so.

This essentially makes you personally liable for the debt. The availability of substantial collateral or a strong personal guarantee can significantly improve your chances of securing a loan, particularly if your business lacks a long and established credit history. For example, a small business owner might offer their home as collateral to secure a larger loan amount, demonstrating their commitment to repayment and mitigating the lender’s risk.

The presence of collateral significantly reduces the lender’s exposure to potential losses.

Managing Loan Repayment

Securing a small business loan is a significant step, but responsible repayment is equally crucial for long-term success. Failing to manage repayments effectively can lead to serious financial consequences, impacting your credit score and the future viability of your business. A well-structured repayment plan, combined with proactive cash flow management, is key to avoiding these pitfalls.Creating a realistic loan repayment plan requires careful consideration of your business’s financial health and future projections.

It’s not simply about meeting minimum payments; it’s about proactively managing your finances to ensure consistent and timely repayments. This proactive approach minimizes risk and allows for flexibility in handling unexpected expenses.

Creating a Realistic Loan Repayment Plan

A comprehensive repayment plan should detail all loan obligations, including principal, interest, and any additional fees. Begin by gathering all relevant loan documents, including the loan agreement, amortization schedule, and any associated paperwork. Next, carefully analyze your business’s monthly income and expenses to determine how much you can comfortably allocate towards loan repayment without jeopardizing essential operational functions.

Consider using budgeting software or spreadsheets to create a detailed financial forecast, projecting income and expenses for the loan’s duration. This forecast should account for seasonal fluctuations, anticipated growth, and potential unexpected costs. Finally, compare your projected cash flow with your loan repayment schedule to ensure a comfortable margin for repayment. If there’s a significant shortfall, explore options such as seeking a loan with a longer repayment period or securing additional funding.

A realistic plan allows for flexibility and reduces the risk of default.

Strategies for Effective Cash Flow Management

Effective cash flow management is the cornerstone of successful loan repayment. Regularly monitor your accounts receivable and payable to ensure timely payments from customers and efficient management of supplier payments. Implement strategies to accelerate invoice payments, such as offering early payment discounts or utilizing online payment systems. Consider negotiating favorable payment terms with suppliers to extend payment deadlines when necessary.

Maintaining accurate financial records is crucial for tracking cash flow and identifying potential problems early. Regularly reconcile bank statements and review financial reports to identify trends and areas for improvement. Budgeting and forecasting tools can help predict future cash flow and identify potential shortfalls before they become critical issues. For example, a restaurant might see a surge in revenue during the holiday season, but careful planning is required to manage cash flow during slower months.

Consequences of Loan Default and Potential Solutions

Loan default can have severe repercussions for your business and personal credit. It can lead to legal action, including lawsuits and wage garnishment. Your credit score will be negatively impacted, making it difficult to secure future loans or credit. Your business may face closure if the lender pursues repossession of assets or initiates bankruptcy proceedings. However, proactive measures can often mitigate these consequences.

If you anticipate difficulty meeting loan repayments, contact your lender immediately to discuss your situation. Many lenders are willing to work with borrowers experiencing financial hardship, potentially offering options such as loan modification, forbearance, or debt consolidation. Early communication is key to preventing a default and exploring potential solutions. For instance, a small bakery facing unexpected rent increases might negotiate a payment plan with their lender to avoid default.

Seeking professional financial advice can also be beneficial in navigating these challenging circumstances.

Business Development and Related Concepts

Securing a small business loan is rarely an isolated event; it’s intrinsically linked to a company’s broader business development strategy. The loan acts as a catalyst, providing the financial resources necessary to implement growth plans and achieve strategic objectives. Effective use of loan capital directly influences a business’s success and long-term viability.The relationship between loan acquisition and business development is symbiotic.

A well-defined business plan, demonstrating a clear understanding of market needs, competitive landscape, and financial projections, is crucial for securing a loan. Conversely, the loan itself empowers the business to pursue development strategies, such as expanding operations, investing in new equipment, or hiring additional staff. This creates a positive feedback loop, where successful implementation of the development plan strengthens the business’s financial position and opens doors for future funding opportunities.

The Importance of Business Ethics in Loan Acquisition and Management

Maintaining high ethical standards is paramount throughout the loan process. Transparency and honesty in financial reporting are essential for building trust with lenders. Misrepresenting financial information, even inadvertently, can severely damage a business’s credibility and jeopardize loan approval. Furthermore, ethical practices in all aspects of business operations demonstrate financial responsibility and increase the likelihood of loan approval and successful repayment.

This includes transparent accounting practices, fair labor practices, and responsible environmental stewardship.

Business Coaching’s Role in Loan Acquisition and Business Growth

Business coaches provide invaluable support in navigating the complexities of the loan application process and fostering business growth. They offer guidance on developing a compelling business plan, identifying funding sources, and managing financial resources effectively. Experienced coaches can assist with strategic planning, market analysis, and operational efficiency, ultimately strengthening the business’s case for loan approval and maximizing the impact of the funds received.

Their expertise extends beyond the loan application itself, encompassing long-term business strategy and sustainable growth.

The Role of a Well-Defined Business Model and Business Strategy in Loan Applications

A robust business model and a clearly articulated business strategy are cornerstones of a successful loan application. Lenders require evidence that the business has a viable plan for generating revenue and repaying the loan. A well-defined business model Artikels the business’s core offering, target market, revenue streams, and cost structure. A comprehensive business strategy details the steps the business will take to achieve its objectives, including market penetration strategies, product development plans, and expansion strategies.

These documents demonstrate to lenders that the business has a clear vision and a well-thought-out plan for utilizing the loan funds effectively.

Business Travel’s Impact on Loan Requirements or Repayment Plans

Business travel expenses, while potentially necessary for growth, can impact loan requirements and repayment plans. Frequent travel may necessitate adjustments to the cash flow projections included in the loan application. Lenders may request more detailed financial forecasts to account for these expenses, ensuring the business can manage its finances effectively even with the added costs of travel. If travel is a significant part of the business model, this needs to be clearly articulated and justified in the loan application.

For example, a sales representative’s travel to meet clients directly impacts their sales potential, and this needs to be demonstrated in the business plan.

Hypothetical Scenario: Business Loans and Company Strategy

Imagine “GreenThumb Gardens,” a small landscaping company, seeking a loan to expand its operations. Their business strategy centers on acquiring a larger fleet of trucks and hiring additional landscaping crews to meet increasing demand. The loan application clearly articulates this strategy, demonstrating how the new equipment and personnel will increase revenue and profitability, ultimately enabling timely loan repayment.

The loan funds are directly tied to the core business strategy, demonstrating a clear connection between the financial resources and the business’s growth objectives. Failure to secure the loan would directly impede their ability to execute this growth strategy and realize their market potential.

Illustrative Examples

Real-world examples can illuminate the complexities and rewards of securing and managing small business loans. Understanding both successful and challenging scenarios helps prospective borrowers make informed decisions and anticipate potential hurdles.Successful businesses often leverage loans strategically for growth, while others face unforeseen difficulties. Examining these contrasting experiences provides valuable insight into navigating the financial landscape of small business ownership.

Successful Loan Utilization for Expansion

Sarah’s handcrafted jewelry business, “Sparkling Gems,” initially operated from her home. High demand led her to seek a small business loan to expand her operations. She secured a $25,000 loan with a favorable interest rate from a local credit union. This funding allowed her to lease a small storefront, purchase specialized equipment (a high-quality jewelry-making bench and display cases), and hire a part-time assistant.

Within two years, her revenue tripled, allowing her to repay the loan ahead of schedule and reinvest profits into further expansion, including an online store and participation in high-profile craft fairs. Her success demonstrates the transformative power of strategic loan utilization for a small business.

Challenges in Managing Loan Repayment

The “Coffee Corner” cafe, a charming local establishment, encountered difficulties managing their loan repayment after experiencing a period of unexpected economic downturn.

- Unexpected drop in customer traffic due to a nearby competitor’s aggressive marketing campaign and a simultaneous road construction project that significantly reduced foot traffic.

- Increased operating costs stemming from rising rent and supply chain issues impacting coffee bean prices.

- Inadequate financial planning and cash flow management leading to insufficient funds to cover loan payments consistently.

- Failure to explore options for loan restructuring or seek guidance from financial advisors during the initial period of financial strain.

These challenges highlighted the importance of proactive financial planning, contingency planning for unexpected events, and open communication with lenders when facing financial hardship.

Financial Projections of a Small Business Securing a Loan

Imagine a bakery, “Sweet Success,” seeking a $10,000 loan to purchase a new oven. Their projected financial statement might look like this:

| Year | Revenue | Loan Payment | Operating Expenses | Net Profit |

|---|---|---|---|---|

| 1 | $30,000 | $1,200 | $20,000 | $8,800 |

| 2 | $40,000 | $1,200 | $22,000 | $16,800 |

| 3 | $50,000 | $0 | $25,000 | $25,000 |

This simplified projection shows increasing revenue and profit, allowing for loan repayment within three years. The projected increase in revenue reflects the anticipated benefits of the new oven, such as increased production capacity and higher quality baked goods. Realistically, such projections should be more detailed, including seasonal variations and potential risks. However, this illustrates a basic scenario where a loan investment leads to a profitable outcome.

Note that this is a simplified model; actual results may vary.

Successfully navigating the small business loan process requires careful planning, thorough research, and a clear understanding of your business’s financial needs. By thoughtfully considering the various loan options, lender types, and financial implications, entrepreneurs can secure the capital necessary for growth and expansion. Remember that choosing the right loan is a critical step towards building a thriving and sustainable business.

Proactive financial management and a well-defined business strategy will significantly increase your chances of securing favorable loan terms and achieving long-term success.

FAQ Summary

What is a good credit score for a small business loan?

While requirements vary by lender, a higher credit score generally increases your chances of approval and secures better interest rates. Aim for a score above 680, but even scores below that may qualify depending on other factors.

How long does the loan application process typically take?

The timeframe can vary significantly depending on the lender and loan type. Expect the process to take anywhere from a few weeks to several months. Faster approvals are often available through online lenders.

What happens if I default on my small business loan?

Defaulting on a loan can severely damage your credit score, potentially making it difficult to obtain future loans. It may also lead to legal action by the lender, including repossession of collateral or wage garnishment.

Can I get a loan with bad credit?

While it’s more challenging, some lenders specialize in loans for businesses with less-than-perfect credit. You may qualify for a loan with higher interest rates or stricter terms.