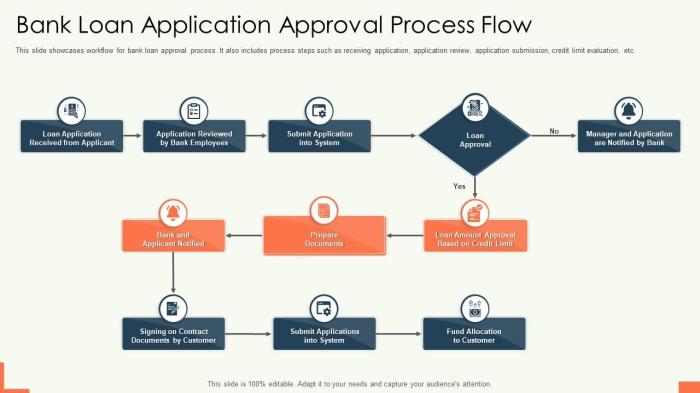

Securing a business loan can be a pivotal moment for any entrepreneur, representing a significant step towards growth and expansion. Navigating the complexities of the application process, however, requires a clear understanding of lender expectations and a well-structured approach. This guide delves into the intricacies of the business loan approval process, providing insights into each stage, from initial application to final approval.

We will explore the critical financial aspects, the importance of a robust business plan, and the impact of ethical business practices on your chances of success.

From preparing compelling financial projections to effectively communicating your business’s value proposition, we’ll cover the key elements that lenders scrutinize. We will also compare and contrast different loan types and highlight strategies for optimizing your application for a favorable outcome. Understanding these elements empowers you to present a strong case, maximizing your chances of securing the funding you need to propel your business forward.

Impact of Business Development, Ethics, and Coaching

Securing a business loan hinges on more than just a strong financial history; it’s about demonstrating a robust and sustainable business model, ethical conduct, and a commitment to growth. Lenders assess the overall health and potential of the business, factoring in not only current financials but also future prospects. This involves examining how the business develops, its ethical foundation, and the strategic guidance it receives.Business development activities significantly influence loan application success.

A well-defined plan showcasing market research, strategic goals, and realistic projections reassures lenders of the business’s viability and potential for repayment. Conversely, a lack of strategic planning or poorly defined goals raises red flags, indicating higher risk.

Business Development Activities and Loan Approval

Proactive business development directly impacts loan eligibility. A comprehensive business plan, including market analysis, competitive strategies, and financial projections, demonstrates preparedness and reduces lender risk. For example, a detailed marketing plan showing anticipated customer acquisition and revenue growth can significantly strengthen an application. Similarly, evidence of successful product or service development, such as positive customer feedback or pilot program results, adds credibility and showcases the business’s potential.

Conversely, a lack of a clear business development strategy, or one that lacks realistic projections, can lead to loan rejection. A business demonstrating consistent growth and a clear path to profitability is far more likely to secure funding.

Ethical Business Practices and Lender Trust

Ethical business practices are paramount in securing financing. Lenders seek assurances that the business operates with integrity and transparency. A history of ethical conduct, documented through compliance with regulations and industry best practices, builds trust and reduces perceived risk. Examples include transparent accounting practices, fair labor practices, and adherence to environmental regulations. Conversely, a history of ethical violations or questionable practices can significantly damage an application’s chances.

A lender’s due diligence often includes investigating a business’s reputation and history, so maintaining a strong ethical profile is crucial. For instance, a business known for its commitment to fair pricing and sustainable practices will likely attract more favorable terms from lenders compared to one with a history of price gouging or environmentally damaging practices.

Business Coaching and Financial Strengthening

Business coaching plays a vital role in enhancing a business’s financial standing and loan eligibility. A skilled coach can provide strategic guidance, improve operational efficiency, and help develop a comprehensive business plan. This, in turn, strengthens the business’s overall financial health and makes it a more attractive prospect for lenders. A coach might help identify areas for cost reduction, improve revenue streams, or develop more effective marketing strategies, all of which contribute to a stronger loan application.

Furthermore, a coach can help the business owner develop essential skills in financial management and forecasting, leading to more accurate and compelling financial projections within the loan application. This proactive approach to business management demonstrates a commitment to growth and financial responsibility, factors lenders highly value.

Impact of Diverse Business Development Strategies

Different business development strategies impact loan eligibility differently. For example, focusing on organic growth through improved operations and customer retention might be viewed more favorably than rapid expansion fueled by high-risk debt. A strategy centered around innovation and technological advancement could attract investors and lenders who are interested in supporting cutting-edge businesses, while a strategy based solely on cost-cutting might indicate a lack of growth potential.

The optimal strategy depends on the business’s specific circumstances and goals, but a well-articulated and realistic plan, regardless of the chosen approach, is crucial for loan approval. A lender will assess the alignment between the chosen strategy, the business’s resources, and the market conditions to gauge the likelihood of success.

Business Loans, Models, Strategies, and Travel

Securing funding for your business can be a crucial step towards growth and success. Understanding the different types of loans available, how your business model impacts the application process, and the role of business travel in your overall strategy are all vital components of a successful funding application. This section will explore these key areas to provide a clearer understanding of how to effectively navigate the process.

Types of Business Loans and Their Characteristics

Businesses have several loan options to choose from, each with its own advantages and disadvantages. The most common types include term loans, lines of credit, and SBA loans. Term loans provide a fixed amount of money for a specific period, with regular repayments. Lines of credit offer a flexible amount of credit that can be drawn upon and repaid as needed, up to a pre-approved limit.

SBA loans, backed by the Small Business Administration, offer more favorable terms and conditions for eligible businesses. The best choice depends heavily on the business’s specific financial needs and risk profile.

Business Models and Loan Applications

The structure and nature of your business model significantly influences your loan application’s success. For example, a well-established, profitable business with a strong track record will generally find it easier to secure funding than a startup with limited operational history. Businesses with predictable revenue streams and strong cash flow are viewed more favorably by lenders. The business plan itself, which should clearly articulate the business model, is a key element in the loan application process.

A comprehensive business plan demonstrates a clear understanding of the market, the business’s competitive advantages, and a realistic financial projection.

Integrating Business Travel into a Business Strategy

Business travel, while involving expenses, can be a critical component of a successful business strategy. It allows for face-to-face meetings with clients, partners, and suppliers, fostering stronger relationships and potentially leading to increased sales and collaborations. Attending industry conferences and trade shows provides opportunities for networking, market research, and staying current with industry trends. Strategic travel can significantly contribute to business growth and should be considered a valuable investment rather than simply an expense.

Justifying Business Travel Expenses in Loan Applications

When including business travel expenses in a loan application, it’s crucial to demonstrate a clear link between the travel and the expected return on investment (ROI). This can be achieved by providing detailed itineraries, outlining the purpose of each trip, and quantifying the potential benefits. For instance, a trip to meet a major potential client should include projections of the potential revenue generated from that client.

Attending a trade show should justify the expense by highlighting the expected number of leads generated and potential sales resulting from the event. Well-documented travel expenses, clearly demonstrating their contribution to business growth, are more likely to be favorably considered by lenders.

Comparison of Business Loan Options

| Loan Type | Pros | Cons |

|---|---|---|

| Term Loan | Fixed payments, predictable budgeting | Higher interest rates, less flexibility |

| Line of Credit | Flexibility, access to funds as needed | Interest rates can fluctuate, potential for high debt if not managed carefully |

| SBA Loan | Favorable terms, lower interest rates | Lengthy application process, stringent eligibility requirements |

Successfully navigating the business loan approval process hinges on a multifaceted approach that encompasses strong financials, a compelling business plan, and ethical business practices. By understanding the lender’s perspective and meticulously preparing your application, you can significantly increase your chances of securing the necessary funding. Remember, a well-structured application demonstrating financial stability, a clear business strategy, and a commitment to ethical conduct builds trust and confidence, paving the way for a successful loan approval.

Popular Questions

What is a credit score, and why is it important?

A credit score is a numerical representation of your creditworthiness. Lenders use it to assess your risk as a borrower. A higher score indicates a lower risk, increasing your chances of loan approval and potentially securing better interest rates.

How long does the loan approval process typically take?

The timeframe varies depending on the lender and the complexity of your application. It can range from a few weeks to several months.

What happens if my loan application is rejected?

If rejected, review the reasons provided by the lender. Address any weaknesses in your application (e.g., improve financial projections, strengthen business plan) and reapply to a different lender or after addressing the concerns.

Can I negotiate loan terms?

Yes, it’s often possible to negotiate interest rates, fees, and repayment terms. Prepare a strong case showcasing your business’s potential and financial stability.