Securing funding is often the biggest hurdle for aspiring entrepreneurs. Small Business Administration (SBA) loans offer a lifeline, providing access to capital that can transform a fledgling idea into a thriving enterprise. Understanding the intricacies of SBA loan programs, however, is crucial for successful application and management. This guide navigates the complexities, offering insights into eligibility, application processes, and effective repayment strategies.

From crafting a compelling business plan to understanding the various loan types and their associated benefits and drawbacks, we’ll explore the entire journey of obtaining and utilizing an SBA loan. We’ll also address common concerns, providing practical advice to maximize your chances of approval and ensure long-term financial health for your business.

SBA Loan Eligibility Requirements

Securing an SBA loan can be a game-changer for small businesses, providing access to capital for expansion, equipment purchases, or navigating challenging economic periods. However, eligibility isn’t guaranteed. Understanding the requirements is crucial for a successful application.

SBA Loan Eligibility Criteria for Small Businesses

To qualify for an SBA loan, your business must meet several key criteria. These requirements are designed to ensure the loan is a sound investment and that the business has a reasonable chance of success. Key factors considered include your business’s age, credit history, revenue, and the purpose of the loan. The specific requirements can vary depending on the type of SBA loan you’re applying for.

Generally, you’ll need to demonstrate good financial standing, a viable business plan, and a clear understanding of how the loan will be used to benefit your business. Furthermore, your personal credit score plays a significant role in the approval process. A higher credit score typically improves your chances of approval and may lead to more favorable loan terms.

Types of SBA Loan Programs and Their Eligibility Requirements

The SBA offers various loan programs, each designed for specific business needs and stages of development. The 7(a) loan is the most common, offering flexible financing for a wide range of purposes. Eligibility generally requires a sound business plan, good credit history, and sufficient collateral. The 504 loan program is designed for larger projects, often involving real estate purchases or major equipment acquisitions.

This program requires a stronger financial foundation and typically involves a third-party lender. Microloans are specifically tailored for smaller businesses with limited access to traditional financing, offering smaller loan amounts and potentially less stringent requirements. Finally, the CDC/504 loan program partners with Certified Development Companies (CDCs) to provide financing for fixed assets, often requiring a strong business plan and a substantial equity contribution.

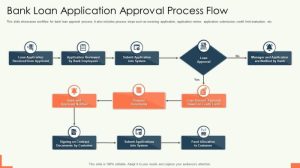

Step-by-Step Guide to the SBA Loan Application Process

Applying for an SBA loan involves several steps. First, you need to carefully research the different SBA loan programs and determine which one best suits your needs. Next, prepare a comprehensive business plan that Artikels your business’s history, financial projections, and the intended use of the loan funds. Gather all necessary financial documents, including tax returns, bank statements, and profit and loss statements.

Then, you’ll need to find an SBA-approved lender. Many banks and credit unions participate in the SBA loan program. Submit your complete application to your chosen lender, who will review your application and conduct a thorough assessment of your creditworthiness and business viability. The lender will then submit your application to the SBA for final approval.

Finally, once approved, you’ll receive the loan funds and can begin using them for your intended business purposes.

Comparison of SBA Loan Programs

| Loan Program | Advantages | Disadvantages | Typical Uses |

|---|---|---|---|

| 7(a) Loan | Flexible, widely available, various uses | More stringent credit requirements, potentially higher interest rates than other programs | Working capital, equipment purchases, real estate |

| 504 Loan | Lower interest rates, longer repayment terms, suitable for large projects | More complex application process, requires significant equity investment | Major equipment, real estate purchases, expansion |

| Microloan | Smaller loan amounts, less stringent credit requirements, easier application process | Limited loan amounts, shorter repayment terms | Working capital, inventory, equipment for small businesses |

| CDC/504 Loan | Access to potentially lower interest rates, longer repayment terms, suitable for fixed assets | Requires working with a CDC, more complex application process | Real estate, major equipment purchases |

Securing SBA Loan Funding

Securing SBA loan funding requires a multifaceted approach, encompassing a well-structured business plan, a meticulously prepared application, and a demonstrably strong financial profile. The process demands careful attention to detail and a clear understanding of lender expectations. Success hinges on presenting a compelling case that showcases your business’s viability and your ability to repay the loan.

The Importance of a Strong Business Plan

A robust business plan serves as the cornerstone of your SBA loan application. It provides lenders with a comprehensive overview of your business, its market position, its financial projections, and its management team. A well-crafted plan articulates your business goals, strategies for achieving them, and a realistic assessment of potential risks and challenges. Lenders use the business plan to evaluate the potential for success and to gauge the applicant’s understanding of their business.

A poorly written or incomplete plan significantly reduces the chances of loan approval. For example, a plan lacking detailed financial projections or a market analysis would be viewed unfavorably.

Preparing a Compelling Loan Application

A compelling loan application goes beyond simply filling out forms. It requires a clear and concise presentation of your business’s financial history and future projections. This includes providing accurate and detailed financial statements, such as profit and loss statements, balance sheets, and cash flow statements for the past three to five years. Your application should clearly articulate the purpose of the loan, how the funds will be used, and a detailed repayment plan.

Strong financial projections, based on realistic assumptions and market research, demonstrate your understanding of your business’s financial performance and your ability to manage debt. For instance, projecting unrealistic revenue growth or ignoring potential expenses will likely result in application rejection.

The Role of Credit Score and Financial Statements

A good credit score and strong financial statements are crucial for SBA loan approval. Lenders use your credit score as an indicator of your creditworthiness and your ability to manage debt responsibly. A higher credit score generally translates to better loan terms and a higher likelihood of approval. Similarly, strong financial statements demonstrate your business’s financial health and stability.

Consistent profitability, positive cash flow, and a healthy debt-to-equity ratio significantly increase your chances of securing funding. A business with a history of losses or high debt levels will face a more challenging approval process. For example, a business with a consistently declining revenue trend and high debt levels would be considered a higher risk.

Required Documents for an SBA Loan Application

A complete SBA loan application requires a comprehensive collection of documents. Failing to provide all necessary documentation can delay the process or lead to rejection.

- Completed SBA loan application form

- Detailed business plan

- Personal and business tax returns (past 3-5 years)

- Financial statements (profit and loss, balance sheet, cash flow statements – past 3-5 years)

- Personal and business credit reports

- Resumes of key personnel

- Legal documents (articles of incorporation, partnership agreements, etc.)

- Collateral information (if applicable)

- Proof of business ownership

Managing SBA Loan Repayment

Successfully navigating SBA loan repayment is crucial for the long-term health of your small business. Understanding your repayment options, proactively managing your cash flow, and taking preventative measures against default are key to ensuring a smooth repayment process and maintaining a positive business credit history. This section will Artikel strategies to help you achieve this.

SBA Loan Repayment Options

The repayment terms of your SBA loan will depend on the type of loan and your lender. However, most SBA loans offer a variety of repayment schedules, typically ranging from several months to 25 years. These schedules are usually structured as monthly installments, with each payment consisting of both principal and interest. Some loans might offer a grace period before repayments begin, allowing you time to establish your business.

It’s essential to carefully review your loan agreement to understand your specific repayment terms and to communicate any potential challenges to your lender early on. They may be able to work with you to adjust the payment schedule if necessary, possibly through deferment or forbearance options.

Strategies for Effective Cash Flow Management

Maintaining a healthy cash flow is paramount for timely loan repayments. A robust budgeting system, carefully tracking income and expenses, and forecasting future cash inflows and outflows are vital. Consider implementing these strategies: Develop a detailed monthly budget that incorporates your loan repayment, anticipate seasonal fluctuations in revenue, and build a financial buffer to cover unexpected expenses.

Explore options to improve your collection process for outstanding invoices, and look for ways to reduce unnecessary operating costs. Regularly review your financial statements and compare them to your budget to identify any discrepancies and address them promptly. Proactive financial management will significantly enhance your ability to meet your loan obligations.

Avoiding SBA Loan Default

Defaulting on an SBA loan can have severe consequences, including damage to your credit score, potential legal action, and even business closure. To avoid default, proactive communication with your lender is crucial. If you foresee any challenges in meeting your repayment schedule, contact your lender immediately. They may be able to offer solutions such as loan modification, deferment, or forbearance.

Furthermore, diligently maintain accurate financial records, regularly monitor your cash flow, and proactively address any potential financial issues before they escalate. Seeking professional advice from a financial advisor or business consultant can provide valuable guidance and support. Remember, early intervention is key to preventing a default.

Resources for Small Business Owners Facing Repayment Challenges

Facing challenges with loan repayment can be daunting, but numerous resources are available to assist small business owners.

- Your Lender: Your first point of contact should be your SBA lender. They are often willing to work with borrowers facing difficulties and may offer restructuring options.

- Small Business Administration (SBA): The SBA website provides a wealth of information, resources, and counseling services for small businesses, including guidance on managing debt.

- SCORE: SCORE provides free mentoring and workshops for small business owners on various aspects of business management, including financial planning and debt management.

- Small Business Development Centers (SBDCs): SBDCs offer consulting services and training programs to help small businesses improve their financial health and manage their debt.

- Financial Advisors and Accountants: Consulting with a financial advisor or accountant can provide personalized guidance and support in navigating financial challenges and developing strategies for debt management.

Impact of SBA Loans on Business Growth

Small Business Administration (SBA) loans can be a powerful catalyst for growth, providing the capital necessary to expand operations, hire employees, and invest in new technologies. Access to these funds can significantly impact a small business’s trajectory, allowing it to compete more effectively and achieve its full potential. However, it’s crucial to understand both the benefits and potential drawbacks before seeking an SBA loan.SBA loans offer a lifeline for many small businesses struggling to secure traditional financing.

The government backing reduces the risk for lenders, making it easier for businesses to obtain loans they might otherwise be denied. This access to capital can be transformative, enabling expansion into new markets, the development of innovative products or services, and overall increased profitability.

Expansion of Operations

Securing an SBA loan can directly translate into tangible business expansion. This might involve purchasing new equipment, increasing inventory, hiring additional staff, or leasing larger facilities. For example, a bakery receiving an SBA loan could invest in a larger oven, allowing them to increase production and meet growing demand. Similarly, a retail business might use the funds to open a second location, expanding its market reach and customer base.

The increased capacity and reach directly contribute to revenue growth and market share expansion.

Challenges in Utilizing SBA Loans for Growth

While SBA loans offer significant opportunities, businesses should be aware of potential challenges. The application process can be lengthy and complex, requiring extensive documentation and financial reporting. Furthermore, the loan terms, including interest rates and repayment schedules, need careful consideration to avoid financial strain. Mismanagement of funds can lead to difficulties meeting repayment obligations, potentially harming the business’s credit rating and future financing prospects.

A thorough understanding of the loan terms and a realistic financial plan are crucial for successful implementation.

Impact Across Industries

The impact of SBA loans varies across different industries. For example, a manufacturing business might use an SBA loan to purchase new machinery, significantly boosting production efficiency and output. A technology startup could use the funds for research and development, creating a new product or service with high growth potential. In contrast, a service-based business might use the funds to hire additional staff or expand its marketing efforts.

The specific application and impact of the loan are tailored to the unique needs and operational characteristics of each industry.

Case Study: Successful SBA Loan Utilization

Consider a small tech firm specializing in sustainable energy solutions. Facing rapid growth but limited access to capital, they secured a 7(a) SBA loan. The funds were used to expand their research and development team, resulting in the creation of a new, highly efficient solar panel technology. This innovation led to a significant increase in sales, attracting larger clients and expanding the company’s market share.

The SBA loan acted as a catalyst, allowing the business to capitalize on its innovative potential and achieve substantial growth. Their strategic use of the loan funds, coupled with a well-defined business plan, resulted in a successful outcome, demonstrating the potential of SBA loans to drive significant business expansion.

Business Development & Related Concepts

Securing an SBA loan is not just about accessing capital; it’s a crucial step in a comprehensive business development strategy. The loan itself acts as a catalyst, enabling businesses to implement growth plans and achieve their long-term objectives. Effective utilization of SBA loan funds requires a clear understanding of business development principles and ethical practices.

The Interplay Between SBA Loans and Business Development Strategies

SBA loans provide the financial resources necessary to execute various business development strategies. This could include expanding operations, investing in new equipment, hiring additional staff, or developing new products or services. A well-defined business plan, outlining specific goals and how the loan funds will be used to achieve them, is essential for securing the loan and demonstrating responsible financial management to the lender.

For example, a bakery securing an SBA loan might use the funds to purchase a larger oven, increasing production capacity and allowing them to fulfill more wholesale orders – a direct implementation of their business development strategy.

The Significance of Business Ethics in SBA Loan Acquisition and Usage

Maintaining high ethical standards is paramount throughout the entire SBA loan process. Transparency and honesty in financial reporting are crucial for building trust with lenders. Misrepresenting financial information or diverting funds for purposes other than those stated in the loan application is not only unethical but also illegal, leading to potential loan default and severe legal consequences. Ethical business practices demonstrate financial responsibility and increase the likelihood of loan approval and successful repayment.

Business Coaching’s Role in Securing and Managing SBA Loans

Business coaching offers invaluable support in navigating the complexities of securing and managing SBA loans. A coach can provide guidance on developing a strong business plan, improving financial forecasting, and refining the loan application process. They can also assist with financial management strategies post-loan approval, ensuring responsible spending and timely repayment. For instance, a coach might help a struggling restaurant owner refine their cost management strategies, improving their profitability and reducing the risk of loan default.

The Importance of a Sound Business Model and Strategy in SBA Loan Success

A robust business model and a well-defined business strategy are fundamental to securing and effectively utilizing SBA loan funds. The business model should clearly articulate the value proposition, target market, revenue streams, and cost structure. The business strategy Artikels the specific steps needed to achieve the business goals, including marketing plans, operational strategies, and financial projections. Lenders assess these elements to determine the loan applicant’s ability to repay the loan and achieve sustainable growth.

A clearly articulated plan demonstrates to lenders a commitment to success and minimizes risk.

The Influence of SBA Loans on Business Travel and Market Expansion

Securing an SBA loan can significantly impact a business’s ability to engage in business travel, particularly for market expansion. The funds can cover travel expenses related to attending industry conferences, meeting with potential clients or partners in new markets, and conducting market research. For example, a software company might use loan funds to send a team to a technology conference in another state to network and showcase their product, potentially leading to significant new business opportunities.

Comparison of Business Loan Options: SBA Loans and Alternatives

Several business loan options exist, each with its own advantages and disadvantages. Traditional bank loans often require stronger credit scores and more collateral than SBA loans. Lines of credit offer flexibility but may come with higher interest rates. Merchant cash advances provide quick funding but can be expensive due to high fees. Compared to these options, SBA loans offer more favorable terms, particularly for businesses with less-than-perfect credit, and often require less collateral.

However, the application process can be more complex and time-consuming.

Illustrative Examples of SBA Loan Use

SBA loans offer crucial financial support for small businesses navigating various challenges and opportunities. The following examples illustrate how these loans can be instrumental in achieving business goals, from overcoming unexpected setbacks to facilitating strategic expansion. Each scenario showcases the versatility and impact of SBA financing.

Overcoming a Financial Challenge with an SBA Loan

Maria’s “The Cozy Corner Cafe,” a charming independent coffee shop in a small town, faced a significant financial hurdle when a sudden, unexpected plumbing failure caused extensive damage to its kitchen and forced a temporary closure. Repair costs were estimated at $25,000, a sum far exceeding Maria’s available cash reserves. Facing potential bankruptcy, Maria applied for an SBA 7(a) loan.

The loan application, supported by detailed financial records and a robust business plan outlining the cafe’s recovery strategy, was approved for $20,000. The funds covered the necessary repairs, allowing The Cozy Corner Cafe to reopen within three weeks. The cafe’s loyal customer base returned, and with careful budgeting and efficient management of the loan repayment, Maria was able to pay off the debt within two years, strengthening the cafe’s financial stability and ultimately bolstering its long-term prospects.

Expansion with an SBA Loan: “Artisan Breads”

Artisan Breads, a rapidly growing bakery specializing in handcrafted sourdough loaves and artisan pastries, secured an SBA 504 loan for $150,000 to expand its operations. The bakery, known for its high-quality products and dedicated customer base, had outgrown its current facility. The SBA 504 loan, which offered favorable terms and a lower down payment compared to conventional financing, enabled Artisan Breads to lease a larger commercial space.

This larger facility allowed for increased production capacity, the addition of new equipment (a high-capacity oven and a commercial-grade mixer), and the creation of a small retail space within the bakery. The expansion resulted in a 40% increase in sales within the first year, solidifying Artisan Breads’ position in the market and creating several new job opportunities.

Equipment Purchase and Productivity Increase: “Green Thumb Gardening”

Green Thumb Gardening, a landscaping company, used an SBA 7(a) loan to purchase a new, state-of-the-art landscaping truck equipped with a hydraulic lift and specialized tools. This truck, costing $45,000, significantly improved the company’s efficiency. The hydraulic lift eliminated the need for manual loading and unloading of heavy equipment and materials, reducing the time spent on each job by an average of 30%.

The specialized tools increased the precision and speed of various landscaping tasks. The financial outcome was impressive: increased efficiency translated to a 20% increase in completed projects within the first year, resulting in a substantial boost to revenue and profitability. The improved efficiency also allowed Green Thumb Gardening to take on more clients, further expanding its market reach and strengthening its position within the competitive landscaping industry.

Navigating the world of SBA loans requires careful planning and a thorough understanding of the process. By diligently preparing a strong application, managing finances effectively, and understanding the long-term implications, small business owners can leverage these valuable resources to achieve sustainable growth and overcome financial challenges. Remember that seeking professional guidance from financial advisors or SBA representatives can significantly improve your chances of success.

Question & Answer Hub

What is the maximum loan amount I can receive through an SBA loan?

The maximum loan amount varies depending on the type of SBA loan program. There’s no single maximum; it depends on factors like your business needs and creditworthiness.

What happens if I miss an SBA loan payment?

Missing payments can negatively impact your credit score and may lead to penalties or even default. Contact your lender immediately if you anticipate difficulties making a payment to explore possible solutions.

Can I use an SBA loan for working capital?

Yes, SBA loans can be used for working capital, but you’ll need to clearly demonstrate how this funding will improve your business’s financial stability and contribute to its long-term success.

How long does the SBA loan application process typically take?

The application process can vary, but it typically takes several weeks to several months, depending on the complexity of your application and the lender’s processing time.